Keller Williams Realty

https://www.buyhomesincharleston.com/blog/5-important-tips-for-insuring-your-home

5 Important Tips for Insuring Your Home

Posted By: Alan Donald In: Home Care TipsDate: Sun, May 31st 2026 1:44 pm

Fast Facts

A Pew Research Center survey conducted in March 2026 found that 71% of homeowners reported having experienced an increase in home insurance costs over the last few years. This is backed up by earlier findings of two studies: A 2025 report by the Consumer Federation of America found that home insurance premiums had increased, on average, by close to 25% between 2021 and 2024, while a Bipartisan Policy Center report released the previous year revealed insurance rates had increased 40% faster than inflation between 2017 and 2022.

(Sources: Pew Research Center, May 2026, Consumer Federation of America, April 2025, and Bipartisan Policy Center, June 2024)

National Insurance Awareness Day Reminds Us to Protect What Matters Most

National Insurance Awareness Day, observed every June 28, reminds us to review our insurance policies to make sure they still provide adequate protection for potential emergencies and natural disasters.

Whether you’re about to buy a home or your current home insurance will be up for renewal, what better time then for us to share this brief overview of home insurance, five important tips for insuring your home – including ways to reduce your premiums, and links to consumer resources available from leading organizations in this sector. Please note that we are not licensed insurance professionals and we ask that you read our disclaimer to that effect at the end of this article.

Overview of Home Insurance

Insurance related to the home is an important form of financial protection for homeowners. In general terms, it helps to cover not only unexpected damage to the dwelling and attached structures, but also loss of personal property within the home, liability expenses for injuries suffered by guests, and certain types of temporary living costs resulting from loss of use after a covered event.

Several types of home-related insurance policies and coverage options are available. The main policy type is commonly referred to as “homeowners” or “hazard” insurance. These standard homeowner policy packages typically bundle the structure and personal contents of single-family homes (HO-3 or HO-5 policies, which differ by covered “perils”), while for condominiums (HO-6 policy) they cover the personal property, liability and the interior walls, floors and ceilings of the unit. Here in the Lowcountry, it is common for standard homeowners policies to also cover wind and hail damage, typically with a different deductible applying for these risks.

Standard policies do not cover all types of risks, most notably some natural disasters.

Most policies do not cover damage derived from rising water (storm surge, flooding). Flood insurance - to protect against rising water - requires a separate policy. FEMA is the federal underwriter for flood insurance (the FEMA policy currently covers up to $250,000 of home value and $100,000 of contents) and private flood insurance providers are also available.

Earthquake coverage for seismic damage can sometimes be added as a rider (or add-on endorsement) to a standard policy. If not, it can be purchased separately. Policies for other specific types of issues, such as sewer backups, service lines and appliance breakdowns, are also available.

Special riders can also be purchased to insure valuable personal property – such as art, collectibles, jewelry and silverware – for their full value when standard policies impose dollar limits for loss or theft.

There is also umbrella insurance to provide broader coverage and higher liability limits than in standard policies.

Landlord insurance, covering the dwelling and lost rental income but not tenant belongings, is essential when renting out a home to long-term tenants. Renters insurance (HO-4 policy) is recommended and normally required for tenants and covers personal property, loss of use and liability, but not the structural building.

Together, these and other types of insurance policies related to the home provide protection and peace of mind, helping to recover from loss due to damage, theft, injury, and liability.

Home insurance needs can change over time, as the values of the home and personal belongings change, as inflation affects construction and medical costs, if the primary use of the home changes, and for other possible reasons.

Updating our insurance coverage to reflect such changes can help provide the protection we need and prevent unexpected financial losses. That’s why it is important to review our existing policy/ies and make regular updates to reflect current values. It’s also why we recommend doing so each year – either when National Insurance Awareness Day comes around each June or before it’s time to renew your policy/ies!

5 Important Tips for Insuring Your Home

Three national organizations – the Insurance Information Institute (III, or Triple-I), the National Association of Insurance Commissioners (NAIC) and the National Association of Realtors (NAR) – provide a range of educational resources on their websites to assist homeowners with insurance. They explain coverage types and share comprehensive guides, insurance shopping comparison tools, home inventory tools and reports on industry trends.

Your state insurance department such as the SC Department of Insurance (SCDOI), major insurance companies, consumer advocacy organizations such as Consumer Reports, and a host of others also share helpful information. (Key webpages have been linked to the highlighted names above.)

Your own local insurance agent and insurance company are also valuable resources that you can reach out to personally.

To help make the important task of insuring your home easier for you, we’ve drawn from these resources to share the following five important tips:

#1: Be aware of needed and available types of insurance coverage for your home and situation: If you have a mortgage on your home, you almost certainly require standard homeowners insurance, as your lender wants to protect “their” asset. Since standard policies do not cover all types of issues, it’s important to identify the range of possible risks unique to your property and situation. For example, do you live in a flood or earthquake zone? Many homes in the Lowcountry lie in flood zones that require flood insurance if you hold a mortgage. Even if it’s not required or you live in a zone with low-to-moderate risk, flood insurance is highly recommended. Earthquake insurance is optional but our region lies within the Charleston Seismic Zone, one of the most seismically active zones in the Eastern United States, so it’s worth considering.

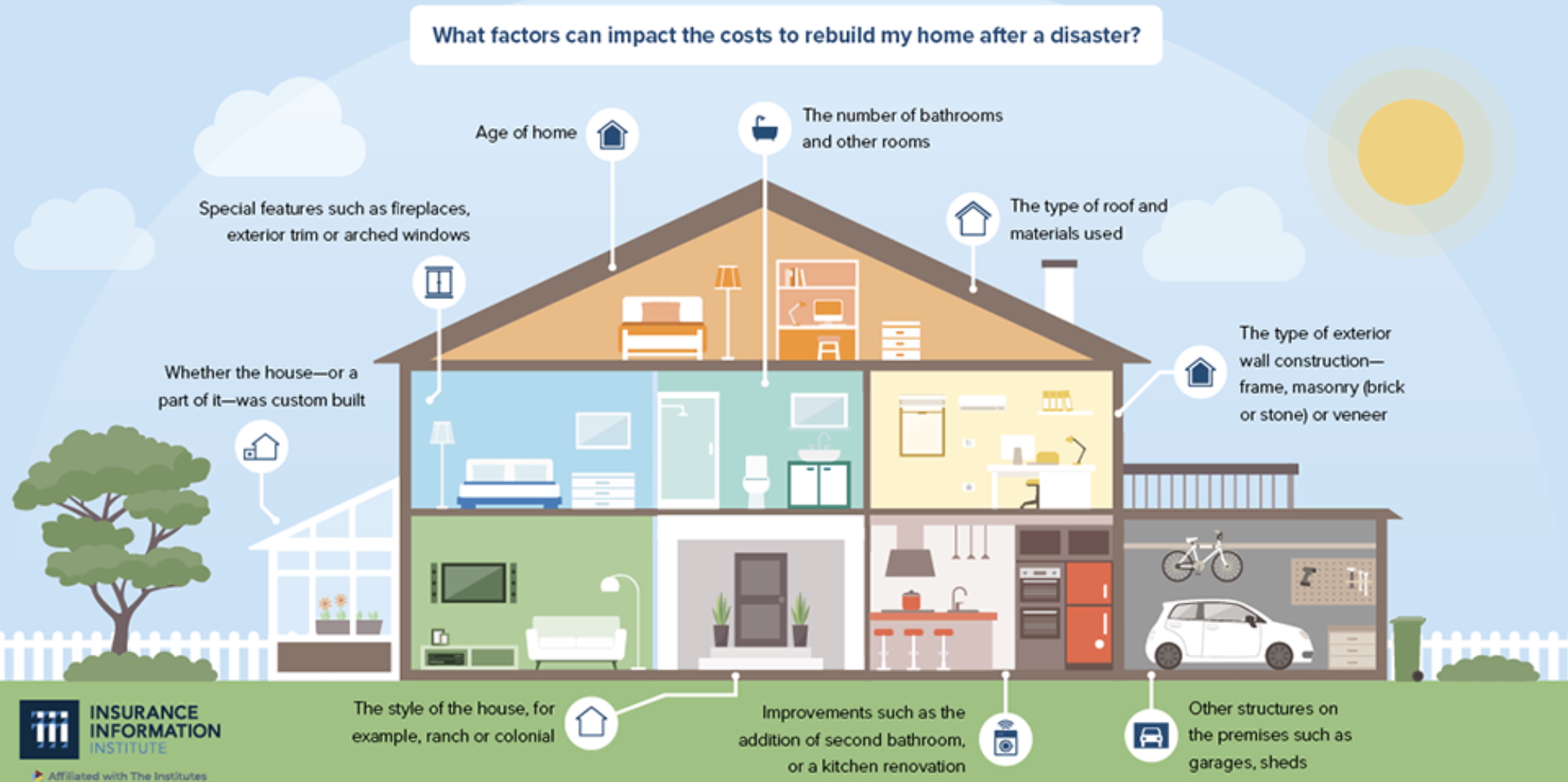

#2: Review your existing coverage and consider updates: To try to avoid being under or over-insured, it’s important to take into account home price appreciation or depreciation in your area, major home improvements you’ve made and changes in your current possessions and household composition (including pets) – and that applies to both recent and planned. Other cost factors should also be considered, such as the age, location, size, condition and disaster risk of your home. Check to see if FEMA has updated the flood map for your area and if your flood risk level has changed. Also make sure you can afford your deductible/s should you experience a loss.

#3: Look for ways to lower your premiums: Rising insurance costs are impacting homeowners across the country, not just locally in the Lowcountry. But there are many ways to reduce your premiums. See if paying your annual premium in full instead of in installments throughout the year can lower its cost. Compare three possible coverage options your insurance provider offers to reimburse you in case of a loss – for actual cash value (ACV), for replacement cost value (RCV) or for guaranteed or extended replacement cost – and how each option could impact your premium. Look into the possibility of adjusting the deductibles and automated values assigned to home contents (provided they comply with any lender guidelines) and how that might impact your premiums. Consider bundling your homeowners insurance with your automobile insurance as well as making improvements to your home that not only help to minimize damage and theft – such as installing storm windows and shutters, home security devices and systems, and storm-resistant roofs – but can also qualify for premium discounts. Maintain good credit and check if membership in certain organizations (e.g., AARP, AAA, alumni associations) provides discounts. Be aware that having a trampoline or swimming pool on the property may increase your premium. Plus, it’s okay to shop around and it costs nothing, so request and compare quotes from other insurance providers. Be sure to take into account their track record and customer service reputation. Recognize that, if you do decide to change providers, there can be waiting periods before coverage comes into force, such as when active named storms are headed towards the Lowcountry.

#4: Be prepared for a possible claim event: Once you have your coverage in place, it’s time to prepare for the unexpected. This will help minimize stress and speed up recovery. Have a disaster preparation plan in place (e.g., storm survival kit, evacuation plan) and have things ready to prepare your home ahead of extreme weather. Establish and maintain an online account with your insurance company/ies, where you’ll have ready access to an electronic copy of your policy and the ability to pay premiums and make and manage claims. Keep your original insurance policy in a secure location such as a safe deposit box and a hard copy in your “Go-bag” in the event of an evacuation. Review and be familiar with the coverage you now have in place. Keep an emergency fund reserve to cover your deductible and more should you experience a loss. Create and keep a summary of improvements made and an inventory of possessions and store them with your policy. Know how to file a claim with your insurance company, what information and documentation will be required, and what the process will be.

#5: Act quickly when you’ve had an event that warrants a claim: If your home does sustain damage that exceeds your deductible, the NAIC advises notifying your insurance company right away. Follow their instructions to file a claim quickly. Take photographs and videos of the damage before cleanup or repairs begin, make a list of all lost items, vet contractors before hiring, save your receipts from emergency repairs, and keep detailed records of all related communications.

Need Help? We’ve Got You Covered

If you’re still unsure about insurance coverage for your home, don’t hesitate to reach out to us.

Protecting you and your home is important to us, and we’re happy to answer basic questions and provide general guidance. But this should in no way substitute for the professional advice of your insurance agent or provider. Nor should you rely exclusively on AI, such as ChatGPT, to obtain the relevant information. Consult an insurance professional before making any important insurance decisions.

We’d be happy to connect you with trusted insurance professionals to help make sure your home coverage needs and questions are adequately addressed.

Disclaimer: The information provided in this article is for general informational and educational purposes only. Real estate agents are not licensed insurance agents or financial advisors. Homeowners insurance requirements, coverage options, and premiums can vary significantly based on the property's location, condition, and the insurance provider. Always consult with a licensed insurance agent or broker to obtain accurate quotes and determine the appropriate coverage for your specific needs.